When you’re able to select from a HELOAN (household collateral financing) and good HELOC (family collateral credit line), first and foremost: done well. You worked hard to create collateral of your home, nowadays you can reap the huge benefits.

Simply how much equity could you borrow against?

With a lot of lenders, you might use as much as 85% of one’s current appraised value of the majority of your home minus the harmony of the financial.

$340,000 [85% of your own residence’s appraised worthy of] – $220,000 [your home loan harmony] = $120,000 [the amount you may be in a position to obtain]

What exactly is a HELOAN?

A house guarantee loan performs such as your financial or other money. Your acquire a quantity, then make typical monthly premiums having a predetermined rate of interest during a predetermined payment period.

What’s good HELOC?

A house guarantee line of credit work similar to a cards credit. You may have a credit limit as you are able to supply when you look at the credit months, that’s normally a decade. Eg a charge card, once you pay off certain otherwise all of everything borrowed, your replace the financing restriction you can obtain away from.You only pay attract on currency you borrow, not the entire limit, and just pay notice once you availableness those funds.

What do HELOANs And you can HELOCs have in common?

For both HELOANs and HELOCs, the rate is normally lower than other sorts of loan cost given that speed is dependant on equity (your house) rather than your revenue and you may credit rating.

For both, you’re in a position to use doing 85% of your own residence’s appraised worthy of without the home loan harmony.

Exactly what distinguishes all of them?

Which have a good HELOAN, you receive the complete count you acquire when you look at the a lump sum. Having an excellent HELOC, you’ve got a borrowing limit and will borrow as often (otherwise as little) of that as you need throughout the latest borrowing label.

Very HELOANs have fixed rates, and more than HELOCs enjoys varying rates of interest. Particular HELOCs (plus those individuals supplied by Financial out-of The united states) offer the option of converting area of the borrowing from the bank line to a fixed price. Footnote dos

Which have HELOANs, you have to pay interest to your whole amount borrowed. Having HELOCs, you pay attract on number of their restriction one you utilize.

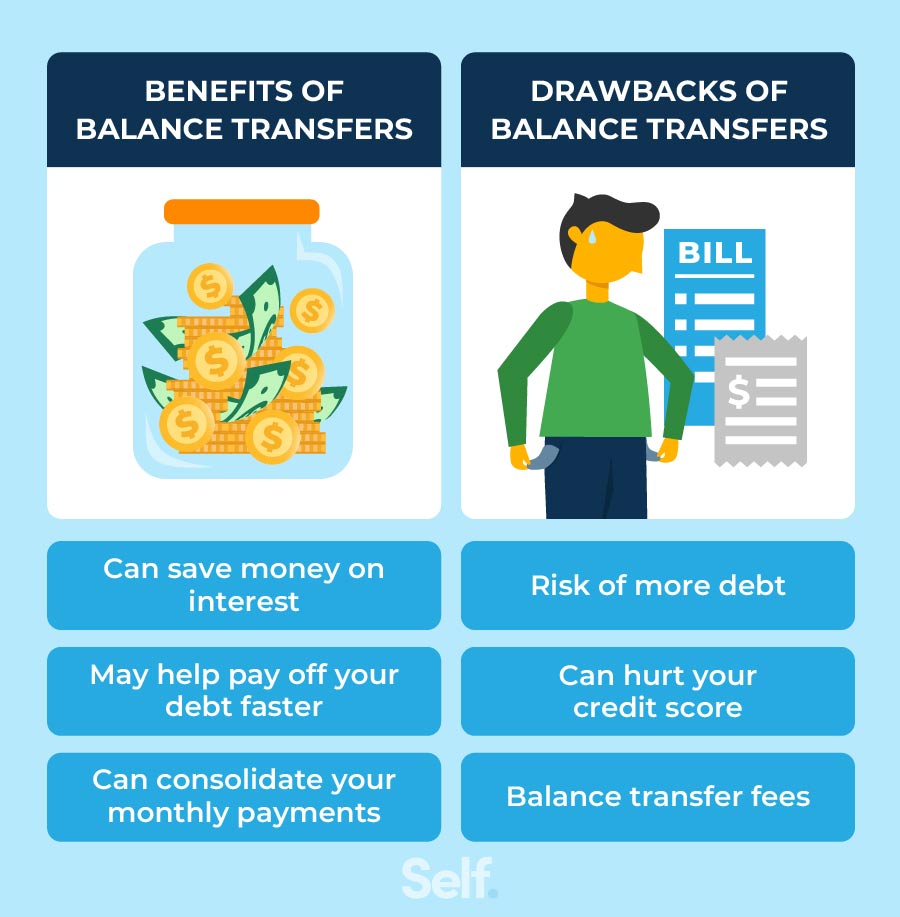

What can you use money from HELOCs and HELOANs getting?

You can use HELOANs and HELOCs to finance home improvement ideas-assuming you will do, the eye tends to be income tax-deductible. Footnote 1

They’re able to be used to have debt consolidation reduction, Footnote 3 crisis will set you back in addition to scientific bills or other unanticipated costs, and degree tuition and you will costs.

Which suits you?

The major deciding points regarding alternatives ranging from HELOAN and you may HELOC is 1) exactly how quickly you can spend the finance, and you can 2) just how certain youre regarding the number it is possible to purchase.

For-instance, whenever you are setting up an out in-soil pond, a beneficial HELOAN most likely the better choice since the you will want the new lump sum of money to cover that venture, and because you are sure that the total price of the project to come of your energy.

If you have made a decision to would a few renovations more than the following years, an excellent HELOC works best since it provides you with the flexibleness so you’re able to simply invest what you would like when you need it. And additionally, you never shell out focus to the money if you do not in reality availableness it.

An email from the lending professional

Should you want to know more about accessing the fresh new guarantee in the your home, I can make it easier to opinion the choices and also money you need.

2 Repaired-Rates Mortgage Solution from the account starting: It is possible to transfer a detachment from your home collateral collection of borrowing (HELOC) membership to the a predetermined-Rate Loan Choice, leading to fixed monthly payments during the a fixed interest. Minimal HELOC number which may be converted in the account beginning to the a fixed-Price Loan Option is $5,000 additionally the restrict amount which is often converted is restricted to ninety% of one’s limit range number. The minimum financing label are one year, as well as the limit name cannot surpass the new account maturity date. Fixed-Price Mortgage Choice during mortgage identity: You are able to move all www.cashadvanceamerica.net/payday-loans-sd of the otherwise a portion of the outstanding HELOC variable-price harmony so you’re able to a fixed-Price Mortgage Choice, resulting in repaired monthly payments within a predetermined interest rate. Minimal an excellent equilibrium that may be converted into a predetermined-Rate Financing Choice is $5,000 regarding a current HELOC membership. Minimal loan identity was 12 months, additionally the limit name doesn’t surpass new membership readiness go out. Just about around three Fixed-Rates Loan Choice is unlock at a time. Cost on the Fixed-Rates Loan Choice are typically higher than varying cost to your HELOC.

3 The fresh cousin advantages of that loan to own debt consolidation reduction count on your personal facts. Including, you can discover desire percentage deals by simply making monthly obligations toward new, straight down rate of interest loan in a price equivalent to otherwise better than what was once paid off with the higher rate loans(s) getting consolidated.