L enders and you will policymakers read the difficult method in which effortless credit in addition to erosion out of underwriting conditions commonly the answer to high need for finance, says Nothaft

Even if you were not area of the household-to order ripple, you were an element of the financial fall out or if you understood people just who destroyed their home in order to a foreclosure or brief income, claims E Mendenhall, chairman of your own Federal Connection regarding Real estate agents and you will a representative with Re/Max Boone Realty inside the Columbia, Mo. As a result, men and women are which have deeper talks ahead of it buy to make sure they will not end losing their house.

Realtors is actually less likely to instantly push people on the most costly home they are able to be eligible for, states Sharga.

We hope users and you will realtors understand the difference between the ability to qualify for a home and capacity to maintain and you may it’s pay for they now, claims Sharga.

One to serious pain enjoys left him or her a great deal more chance averse, thus lenders become more careful whenever taking investment to help you consumers and you may in order to developers, claims Herbert. Meanwhile, the audience is seeing houses starts below they must be, which is an indication of chance aversion certainly developers.

This new crisis continues to be on the vanguard of brains regarding everyone in the lending globe and you will impacts the choices, states Michael Fratantoni, captain economist of your own Financial Lenders Relationship in Arizona.

A few of the products which started the brand new crisis commonly up to and new techniques one been it is actually severely restricted, claims Fratantoni.

Some of those residents who destroyed their home to a short sale or foreclosure, on thirty-five percent have ordered several other family, predicated on CoreLogic.

That means that 65 percent don’t get back, claims Frank Nothaft, master economist during the CoreLogic in the Arizona. Do not fully know as to the reasons those individuals has yet , purchasing once again otherwise what kind of long-long-term impression that keeps.

The fresh credit rules

Lower paperwork and you can interest-merely fund was indeed okay because a tiny niche to possess otherwise qualified individuals which have specific things, claims Nothaft. The challenge are that these high-risk fund turned available everywhere in order to subprime consumers.

Today someone remember that funds must be green, otherwise visitors seems to lose, claims Nothaft. A property foreclosure affects families, groups, lenders and people.

When you find yourself legislation such Dodd-Frank altered new monetary community, lenders and you will investors also destroyed the urges to own chance and https://paydayloanalabama.com/excel/ have changed its choices, says Sam Khater, captain economist off Freddie Mac in McLean, Virtual assistant.

Appraisers common a few of the fault to own overinflated home values while in the new casing growth, simply since the lenders were able to privately communicate with appraisers the standard having a property valuation to match escalating prices.

Statutes are in lay today to get a great firewall involving the appraisal techniques therefore the underwriting process, states James Murrett, president of one’s Assessment Institute and an executive managing director out-of Colliers Global Valuation Corp. within the Hamburg, N.Y.

Which is partially as investors don’t have trust about program, states Herbert. Thus particular consumers that simply don’t easily fit in the standard field could possibly get still not be able to get borrowing from the bank.

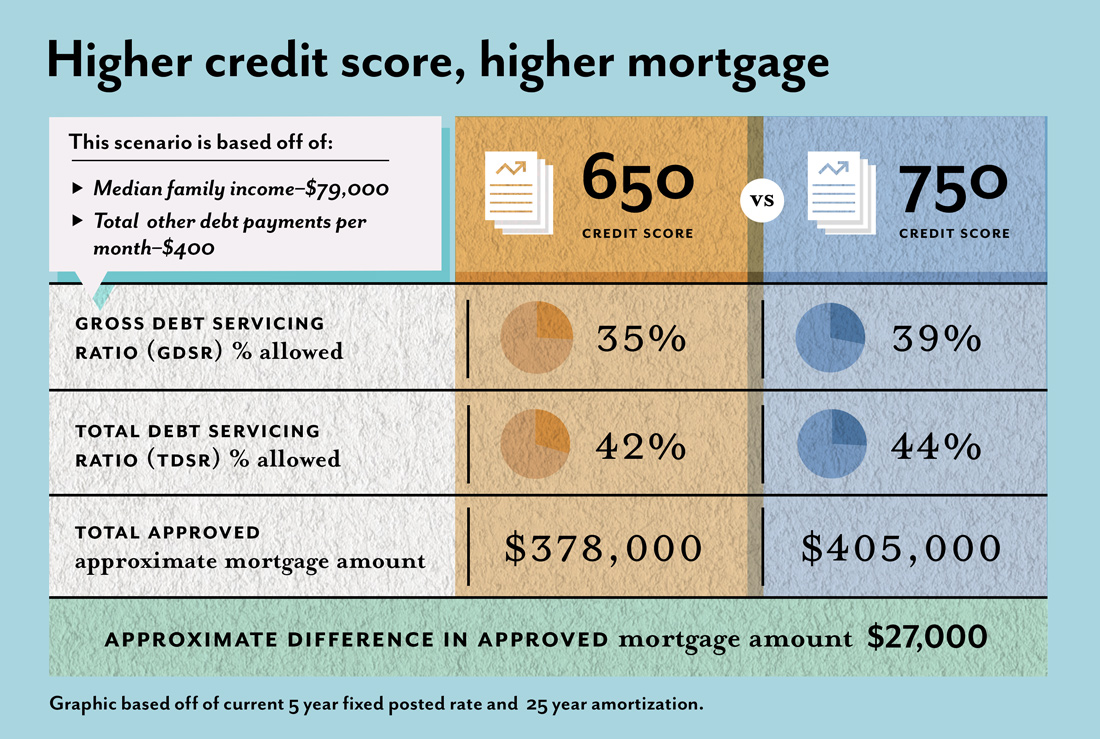

At the top of your construction growth, borrowers with a credit rating out of 620 to 640 qualified for a decreased interest rates for the conventional finance. Credit scores to possess FHA borrowers was basically throughout the mid-500s. By comparison, in the , predicated on Ellie Mae, home financing analytics business, 70 % of individuals got a great FICO rating more 700. The typical FICO rating for conventional finance to possess a house get into the is actually 751, more than 100 affairs greater than that was noticed value a knowledgeable mortgage costs regarding 2004 in order to 2006.